Agentic Regulatory Compliance Copilot for Student Loan Lifecycle Management

How do recent tax law changes affect my student loan repayment strategy?

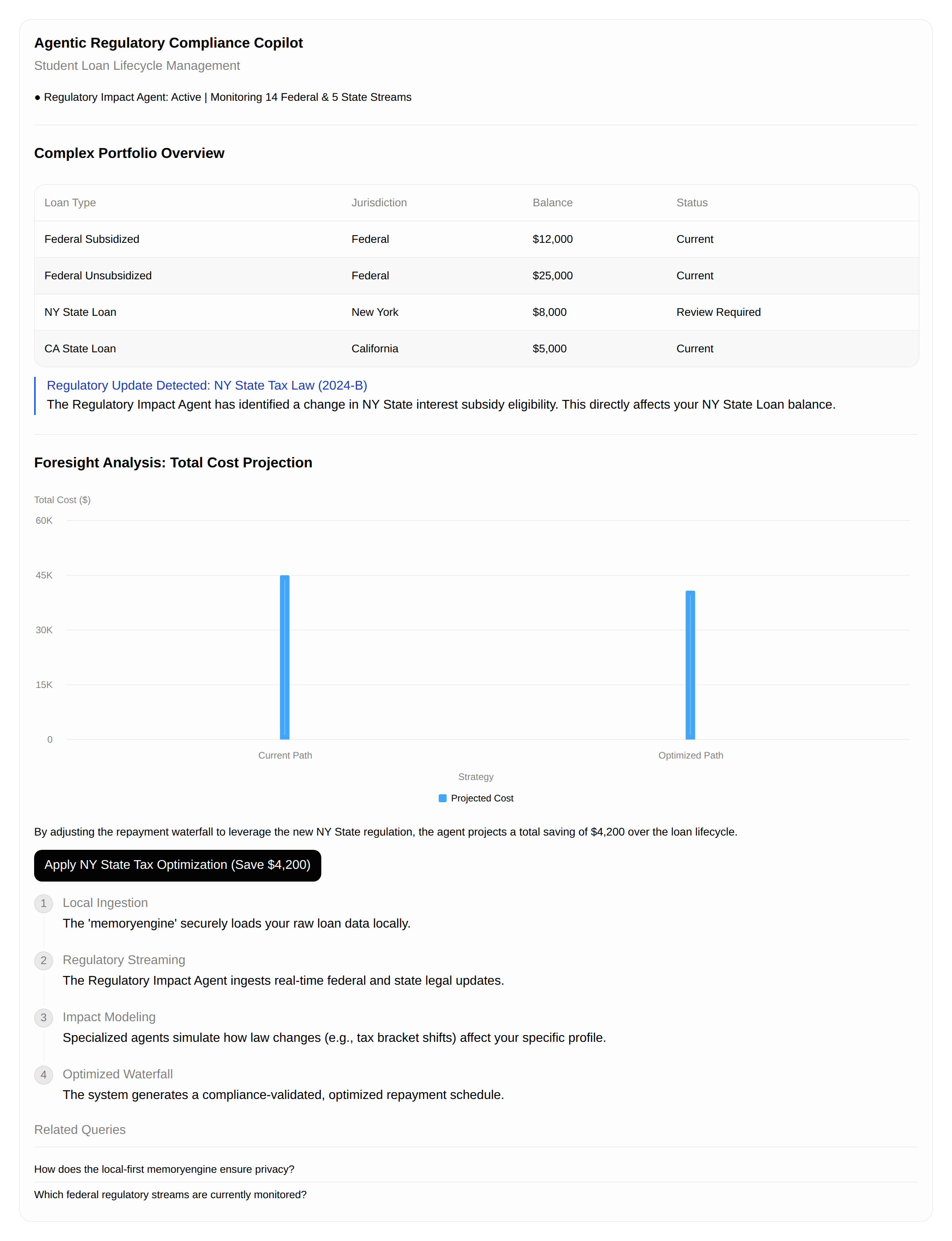

A specialized agent system continuously models how changes in federal and state regulations impact your student loan repayment calculus. It ingests regulatory updates and calculates how shifts in tax law alter your optimal repayment waterfall, generating compliance-validated and financially optimized strategies. This moves beyond static loan calculators to provide foresight on how changing regulations require adjusting your repayment plan.

Process flow

Who it's for

Graduates with complex, multi-state, or federal student loan portfolios who are highly sensitive to regulatory changes (e.g., those anticipating career moves or tax bracket changes).

Why they need it

The true pain point is not budgeting, but regulatory risk. Current tools treat loans as static inputs. When a major law changes (e.g., tax code updates, income verification rules), the entire repayment model breaks or becomes suboptimal, requiring manual consultation with expensive financial advisors.

What it is

A multi-agent, local-first intelligence platform that ingests raw loan data and streams/ingests structured regulatory updates. It runs specialized agents to model the impact of external legal/economic variables on the user's loan repayment calculus, proposing compliant, optimized pathways.

How it works

The system uses the 'memoryengine' for raw loan data. The core innovation is the 'Regulatory Impact Agent,' which ingests structured regulatory text/APIs. It then uses specialized prompt engineering (guided by external financial/legal libraries) to calculate how a change in law (e.g., 'If tax bracket shifts from X to Y, the effective interest rate changes by Z') alters the optimal repayment waterfall. The output is a compliance-validated and optimized schedule.

Differentiation

Unlike general budgeting apps or standard loan calculators that assume static variables, our system models the rate of change of the financial landscape itself. The gap is the lack of a single platform that synthesizes live, external regulatory data streams and applies them to a user's unique, multi-product financial profile to generate proactive compliance advice. This moves beyond calculation to foresight.

Implementation sketch

- Integrate raw loan statements into the 'memoryengine' context store.

- Develop a proof-of-concept 'Regulatory Impact Agent' focused only on one specific, high-friction regulatory area (e.g., federal tax deduction changes related to education).

- Build a focused workflow: Manually feed the agent a recent, complex regulatory document (e.g., IRS guidance PDF) and task it with deriving 3 concrete, actionable changes to the user's existing repayment plan.

First step: Identify 3 specific, high-impact, and complex regulatory changes that occurred in the last 18 months regarding student loans or tax law. For each, manually write a detailed prompt defining the required calculation/impact assessment for the 'Regulatory Impact Agent' to solve.

Remaining risks

- Regulatory Ambiguity and Scope Creep: The system's reliance on ingesting and interpreting complex, evolving legal/regulatory text (e.g., IRS guidance, state statutes) is inherently brittle. A single misinterpretation of a nuanced clause, or the inability to parse a novel legal document format, could lead to providing dangerously incorrect or non-compliant financial advice. — Restrict the initial scope to a single, well-defined, and mathematically unambiguous regulatory domain (e.g., only the interaction between federal tax code changes and interest capitalization for a specific loan type) and build a verifiable knowledge graph layer before the LLM inference layer.

- Data Ingestion Failure (The 'MemoryEngine' Black Box): The core value hinges on combining raw, unstructured user data (loan statements) with structured, external regulatory data. If the 'memoryengine' fails to maintain data integrity, correctly map variables (e.g., matching a specific loan ID across multiple state filings), or if the regulatory data source is unreliable, the entire compliance model collapses, leading to a complete loss of user trust. — Implement a mandatory, human-in-the-loop validation step for all initial data ingestion and for any proposed 'compliance-validated' schedule change, treating the AI output as a draft recommendation requiring expert review.

- Jurisdictional Overload and Maintenance Cost: Financial regulation is not static; it changes constantly across federal, state, and local levels. Maintaining the 'Regulatory Impact Agent' to keep pace with continuous, overlapping legal changes (e.g., a state passing a law that contradicts a federal guideline) creates an unsustainable, perpetual operational overhead far exceeding the scope of an MVP. — Market the product not as a 'real-time compliance engine,' but as a 'Regulatory Change Impact Simulator' that requires the user or a paid partner to feed in the specific regulatory change document, thus limiting the system's responsibility to interpretation rather than continuous monitoring.

Watch for: Any indication that potential users are more concerned with the difficulty of providing the necessary regulatory data (e.g., needing to upload PDFs from multiple state departments) than they are with the potential savings. This signals that the friction point is data acquisition, not regulatory complexity. Kill criterion: If, after initial testing, the system cannot reliably and provably calculate the impact of a single, known, recent regulatory change (e.g., a specific tax deduction adjustment) across two different loan products, the concept is too fragile for a product launch.

Sources the council used

Real-world evidence that grounded this idea — judge it for yourself.