AI-Driven Accounts Receivable Optimization Engine

Which of my outstanding invoices are most likely to go unpaid?

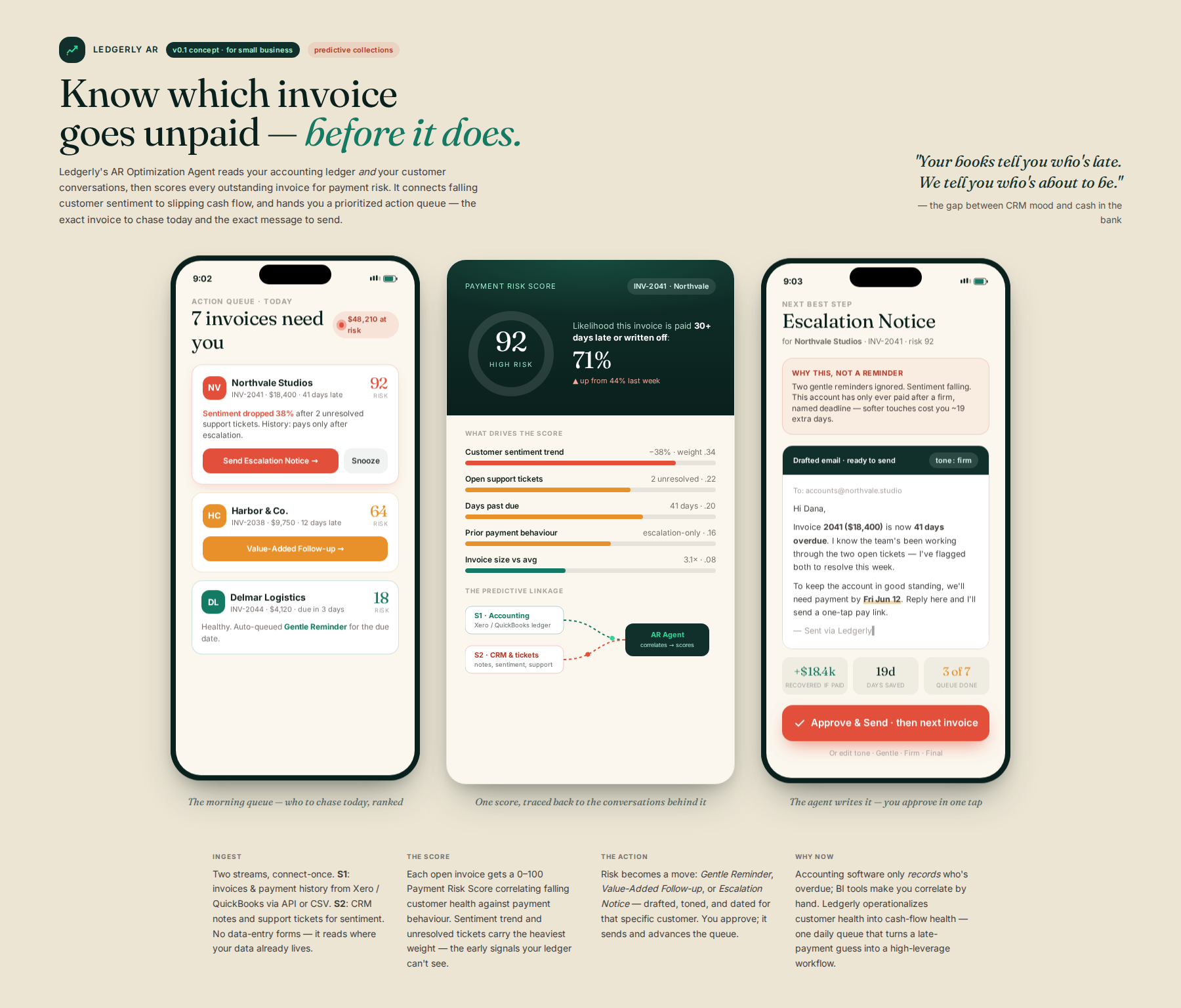

An AI platform analyzes your invoice data alongside customer interaction history to calculate a Payment Risk Score for each outstanding invoice. It correlates structured financial records (from accounting software) with unstructured customer feedback to identify high-risk invoices, then generates a prioritized action queue with personalized communication templates. This bridges CRM and accounting data to operationalize customer health into cash-flow health.

Process flow

Who it's for

Small business owners whose cash flow is critically dependent on timely invoice payments (e.g., service providers, agencies, small manufacturers).

Why they need it

Many small businesses lose significant capital due to poor accounts receivable (AR) management. Current tools are either basic invoicing software (recording transactions) or high-end ERPs that require dedicated finance staff to analyze churn risk—neither offers proactive, predictive payment intervention.

What it is

A focused 'AR Optimization Agent' that ingests structured invoice data (CSV/API) and unstructured customer feedback (e.g., low sentiment from CRM notes) to calculate a 'Payment Risk Score' for every outstanding invoice, then auto-generates the next best communication step (e.g., 'Gentle Reminder,' 'Value-Added Follow-up,' or 'Escalation Notice').

How it works

The system ingests two primary data streams: 1) Structured financial data (Invoices, payment history from Xero/QuickBooks). 2) Unstructured customer interaction data (CRM notes, support tickets). The core agent layer correlates these to generate the Payment Risk Score. The output is a prioritized 'Action Queue' showing which invoices need attention today and the exact recommended communication template/action.

Differentiation

Unlike standard accounting software that only records overdue invoices, or general BI tools that require manual correlation, this product focuses solely on the predictive linkage between customer satisfaction/interaction history and payment behavior. It operationalizes 'customer health' into 'cash flow health,' providing a single, immediate, high-leverage workflow that bridges the gap between CRM data and accounting records.

Implementation sketch

- Phase 1 MVP: Focus exclusively on ingesting invoice/payment data and a limited set of unstructured notes (e.g., last 3 support tickets per client). Build the Payment Risk Scoring model.

- Phase 2: Develop the 'Action Queue' output, allowing users to approve and deploy pre-written, tone-adjusted communication templates directly linked to the risk score.

- Phase 3: Expand data sources to include sales pipeline data to predict future AR issues before they materialize.

First step: Draft a minimal viable data schema and workflow diagram detailing the required inputs (e.g., Client ID, Invoice Amount, Due Date, Last 3 Support Ticket Summaries) and the desired output JSON structure for the 'Action Queue' report.

Remaining risks

- Data Ambiguity and Schema Drift: Real-world financial data (QuickBooks, Xero) and CRM notes are notoriously inconsistent. Schema drift (e.g., a field name changing, required fields being added/removed) will break the ingestion pipelines, causing the core 'Payment Risk Score' calculation to fail silently or produce garbage results. — Implement robust, version-controlled ETL/ELT layers with mandatory data validation checks at ingestion. Build a 'Data Health Dashboard' that alerts the user before the risk score is calculated if source data quality falls below a predefined threshold (e.g., >10% missing required fields).

- The 'Black Box' Problem in Scoring: The predictive link between unstructured sentiment and quantitative payment behavior is opaque. If the model generates a high-risk score, the user will demand to know why (e.g., 'Was it the tone of the last ticket, or the size of the invoice?'). If the explanation is just 'The model says so,' adoption will halt. — Force the model to generate feature attribution alongside the score. The output must explicitly list the top 2-3 contributing factors (e.g., 'Risk increased due to: 1. 30-day aging bucket (Weight: 0.4); 2. Negative sentiment in support ticket summary (Weight: 0.3)').

- Over-reliance on Correlation vs. Causation: The system might identify strong correlations (e.g., 'Low sentiment correlates with delay'), leading the user to treat the output as guaranteed cause-and-effect. This can lead to poor real-world decisions if the underlying relationship is spurious. — Mandate clear, non-technical disclaimers within the 'Action Queue' output, framing the score as a 'Probability Indicator' or 'Suggested Focus Area,' not a definitive prediction. The system must guide the user toward human judgment.

Watch for: A key customer segment (e.g., agencies) expressing frustration that the suggested 'Action Queue' templates feel generic and fail to capture the nuanced, personal relationship required for high-value B2B collections. Kill criterion: If the initial pilot group cannot successfully map the Payment Risk Score to a measurable, positive change in Days Sales Outstanding (DSO) within 90 days, the core predictive hypothesis linking sentiment to payment delay is invalid, and the product must pivot to a purely deterministic, rules-based workflow.

Sources the council used

Real-world evidence that grounded this idea — judge it for yourself.